Australian Living Sectors Market Analysis for European Private Credit

by Investment Analysis Team, Research

Australian Living Sectors Market Analysis for European Private Credit

Executive Summary

Australia's Build-to-Rent (BTR) and Purpose-Built Student Accommodation (PBSA) sectors present notable characteristics for European private credit funds to consider. These sectors are primarily driven by a severe, structural housing supply deficit, robust demographic growth, and increasing government support aimed at alleviating housing pressures. Both sectors exhibit characteristics that may appeal to institutional investors, including stable, long-term, and inflation-linked income streams derived from professionally managed assets.

The BTR sector, while nascent, is poised for significant expansion, underpinned by recent federal tax concessions such as a reduced Managed Investment Trust (MIT) withholding tax rate (from 30% to 15%) and accelerated capital works depreciation (from 2.5% to 4%). These are complemented by streamlined Foreign Investment Review Board (FIRB) approvals and reduced fees for foreign investors.1 The PBSA sector is experiencing a rapid post-pandemic recovery, fueled by a strong rebound in international student arrivals and a substantial national undersupply of beds, estimated at 200,000.3 Melbourne, in particular, stands out as a global education hub with a significant demand-supply imbalance.3

The persistent undersupply in both BTR and PBSA translates into high occupancy rates and consistent rental growth, making them resilient asset classes. Government policy is increasingly supportive, actively incentivizing institutional investment to address the broader housing crisis.1 However, challenges for BTR include its early market stage, the persistent 10% Goods and Services Tax (GST) leakage on development costs, and potential complexities arising from restrictions on tiered trust structures for tax concessions.1 For PBSA, considerations include potential policy shifts impacting international student enrolments and the ongoing pressures of high construction and operational costs.3 Furthermore, macroeconomic factors such as interest rate differentials between Australia and Europe, and Australian dollar (AUD) exchange rate volatility, introduce additional considerations for European investors.7

European private credit funds may consider direct lending facilities as a primary entry mechanism, leveraging the growing Australian private credit market.9 Partnerships with experienced Australia-based firms could be valuable for deal origination, robust due diligence, and navigation of local market nuances and regulatory frameworks.11 Implementing sophisticated currency hedging strategies would be essential to mitigate AUD/EUR exchange rate volatility and protect EUR-denominated returns.12

1. Introduction: Australia's Living Sectors - A Strategic Overview

1.1 Investment Thesis: Why Australian BTR and PBSA?

Australia is currently grappling with a significant housing supply crisis, particularly evident in its major metropolitan centers such as Sydney, Melbourne, and Brisbane. This structural undersupply has led to sustained rental growth and historically low vacancy rates across the residential market, creating an urgent and compelling need for new, purpose-built rental assets.3 This environment positions both Build-to-Rent (BTR) and Purpose-Built Student Accommodation (PBSA) as institutional-grade assets that may deliver stable, long-term, and often inflation-linked income streams. For private credit funds seeking resilient asset classes with predictable cash flows, these characteristics may be of interest.10

The appeal of these sectors is further amplified by robust demographic tailwinds. Australia's overall population growth is strong, significantly driven by net overseas migration, which disproportionately adds to the working-age adult population and, consequently, to housing demand.18 Concurrently, the nation's student population continues to expand, particularly with the post-pandemic rebound in international student arrivals, creating a consistent demand base for specialized accommodation.4

Recent shifts in Australian government policy are actively encouraging and facilitating institutional capital inflows into these sectors. The introduction of specific tax incentives, coupled with streamlined foreign investment processes, signals a more favorable and stable regulatory landscape for long-term investment in BTR and PBSA.1

Australia's traditional residential market has historically been characterized by a strong build-to-sell model and a fragmented private rental sector. This fragmentation is largely dominated by small-scale individual investors, whose primary motivation often revolves around capital gains from property sales rather than long-term rental income.22 This traditional model has proven insufficient to effectively address the escalating housing affordability crisis and the persistent undersupply of rental dwellings.1 In response to these systemic challenges, the Australian government has deliberately pivoted towards promoting large-scale institutional investment in BTR and PBSA. This strategic shift is clearly evidenced by the introduction of targeted tax concessions, such as the reduced Managed Investment Trust (MIT) withholding tax, significant reductions in Foreign Investment Review Board (FIRB) fees, and the strategic linking of increased university international student intake to the provision of new student housing by those institutions.1 This represents a fundamental, long-term policy commitment to fostering these institutional "living sectors" as a critical component of the national housing solution, rather than a short-term or ad-hoc measure. For European private credit funds, this translates into a more predictable and supportive regulatory environment over their investment horizon, potentially reducing policy-related risks. It also suggests that future government initiatives are likely to continue supporting supply-side solutions in these specific areas, further de-risking long-term investments.

1.2 Target Audience: European Private Credit Funds and Direct Lending

This report is specifically tailored for European private credit funds. These funds typically seek investment opportunities that offer higher yields compared to traditional investment-grade bonds, provide floating interest rates as a natural hedge against inflation, and contribute to portfolio diversification with lower correlation to public market fluctuations.10

Direct lending in the Australian real estate market aligns well with these objectives. It provides funds with the flexibility to structure customized deals and access capital in situations where traditional banks may be less active. This reduced activity from major banks is largely a consequence of increased regulations and higher capital requirements implemented following the Global Financial Crisis (GFC), which made it harder for them to extend certain types of loans.10

1.3 Report Scope and Objectives

This report provides a comprehensive and in-depth analysis of the Australian BTR and PBSA investment landscape. It covers critical aspects including current market dynamics, robust growth forecasts, a balanced assessment of benefits and risks, detailed insights into financing structures (specifically direct lending), the influence of key macroeconomic factors, and the impact of government support policies. The primary objective is to equip European private credit funds with the necessary actionable insights and a thorough understanding to confidently evaluate and pursue direct lending opportunities within these promising Australian real estate sectors, facilitated by an Australia-based partner firm.

2. Australian Build-to-Rent (BTR) Sector Analysis

2.1 Definition and Core Characteristics

Build-to-Rent (BTR) is a distinct residential development model where developers and their financiers construct multi-unit buildings with the explicit intention of retaining ownership and renting the units to tenant households, rather than selling them individually.1 While rents may be set at market rates, BTR projects can also incorporate affordable or social housing components, offering units at a discount to market rents.24

A hallmark of BTR is the presence of professional, on-site property management teams. These managers view themselves as providers of long-term rental services to "customers," a fundamental departure from the traditional model where property owners' main income often derives from capital gains upon selling the property.1 This professional approach fosters a number of tenant-friendly benefits, including the provision of long, stable leases, which allows tenants to establish roots in a neighborhood, and greater flexibility regarding pets or minor aesthetic changes to apartments.24 Furthermore, BTR properties are typically maintained to a higher standard, as the owners retain long-term responsibility for the buildings and have a vested interest in their ongoing quality and operational efficiency.24 This long-term ownership perspective also provides strong financial incentives for designing and constructing more sustainable and energy-efficient housing, which in turn attracts and retains quality tenants.24

BTR developments are versatile, capable of catering to a diverse tenant base ranging from high-end luxury products to affordable housing units. These affordable units are often integrated as components of larger, mixed-use developments, sometimes supported by inclusionary zoning laws or government subsidies.24

Australia's traditional private rental market is largely composed of dwellings owned by small-scale investors, whose primary motivation is often capital gains from property sales rather than long-term rental income.22 This model can lead to less stable tenancies, inconsistent property management, and often a reactive approach to maintenance. In stark contrast, the BTR model fundamentally shifts this dynamic by professionalizing landlord services, focusing on tenant retention, and ensuring higher maintenance standards due to the developer's long-term ownership.1 This inherent focus on providing "more tenant-friendly" housing24 through features like long, stable leases, pet policies, and proactive maintenance directly addresses common pain points in the traditional rental market. For investors, this translates into lower tenant turnover25, leading to more predictable occupancy rates and stable cash flows, which significantly de-risks the investment from an operational perspective. It also positions BTR as a preferred option for renters seeking stability and quality, enhancing its long-term viability and attractiveness.

2.2 Market Size and Growth Forecasts

The Australian BTR sector is currently relatively small but is experiencing rapid growth. A 2022 report from Ernst and Young (EY) identified the sector as being worth $16.87 billion, comprising approximately 0.2% of the total value of the residential housing sector, and equating to 23,000 apartments either completed or in development at that time.24

More recent data from JLL as of Q4 2024 indicates there were 9,180 operational BTR apartments, with 4,147 units completed in 2024 alone.9 A further 8,199 units are currently under construction, with 4,635 projected for completion in 2025.9 The total BTR pipeline, including planning approvals, stood at 42,812 apartments as of Q4 2024, representing a 10.5% year-on-year increase.9 Overall, 2025 projections indicate 5,928 completions, a forecasted increase of 21.5%.26 Geographically, Victoria dominates Australia's BTR project pipeline, accounting for 52% of units, followed by Queensland (24%) and New South Wales (17%).9

Historically, Australia's BTR industry lagged behind other developed markets due to regulatory headwinds, including a lack of competitive tax incentives and cumbersome Foreign Investment Review Board (FIRB) approval processes.1 However, the recent passage of the BTR Bill in late 20242, which introduced significant tax concessions (reduced MIT withholding tax and accelerated depreciation), is explicitly identified as a key factor that "should stimulate BTR market activity in 2025".9 The observed and projected growth figures, such as the 21.5% increase in completions forecasted for 202526 and the 10.5% year-on-year rise in the total pipeline9, directly follow these regulatory changes. This strong correlation suggests a direct causal link between proactive government policy and the acceleration of market growth. The "lagging" status1 is being actively addressed, indicating that the sector is transitioning from its nascent stage into a period of more rapid and sustained development. For private credit funds, this implies an increasing volume of viable deal flow and a maturing market, although it is important to acknowledge that the overall scale still remains small compared to more established global markets like the US and UK.1 This also suggests a more predictable policy environment for future investments.

Table 1: Australian Build-to-Rent Market Overview

| Metric | Value/Status | Source |

|---|---|---|

| Current Market Value (2022) | $16.87 billion | 24 |

| Market Penetration (relative to total residential housing) | ~0.2% | 1 |

| Comparison: US BTR Market Penetration | 12% | 1 |

| Comparison: UK BTR Market Penetration | 5.4% | 1 |

| Completed/Operational Units (2022) | 3,900 | 24 |

| Operational Units (Q4 2024) | 9,180 | 9 |

| Units Completed (2024) | 4,147 | 9 |

| Units Under Construction (Q4 2024) | 8,199 | 9 |

| Units in Planning Pipeline (Q4 2024) | 17,043 | 9 |

| Total BTR Pipeline (Q4 2024) | 42,812 apartments | 9 |

| Year-on-Year Growth in Total Pipeline | 10.5% (to Q4 2024) | 9 |

| Forecasted Completions (2025) | 5,928 (21.5% increase from 2024) | 26 |

| Dominant State in Pipeline | Victoria (52%), followed by Queensland (24%) and NSW (17%) | 9 |

Note: Data points are sourced from various reports and may reflect different reporting periods within the specified years.

2.3 Key Benefits for Investors

Investing in the Australian BTR sector offers several compelling advantages for private credit funds:

Stable, Long-Term Cashflows and Professional Management: BTR projects are inherently designed to generate consistent rental income over extended periods. This is underpinned by the operational model that prioritizes professional, on-site management teams whose primary objective is tenant retention. This focus leads to longer lease arrangements, resulting in steady cashflows and stable long-term returns for investors.1 This contrasts favorably with the often less predictable income streams from properties owned and managed by small-scale private investors, who may have shorter investment horizons or less sophisticated management practices.24

Addressing Australia's Housing Supply Shortfall: Australia is currently in the midst of a severe housing crisis, particularly in its major population centers. The National Housing Finance and Investment Corporation (NHFIC) forecasts a significant shortfall of 106,000 residential dwellings by 2026. In response, the Australian government has set an ambitious target to build 1.2 million homes by the end of the decade, underscoring the urgent and substantial demand that BTR developments are uniquely positioned to help address by adding large-scale, professionally managed rental stock to the market.1

Federal and State Tax Concessions: A comprehensive suite of government incentives has been introduced to stimulate BTR investment:

Streamlined FIRB Approval Process: As of May 1, 2024, foreign investors gained the ability to purchase established BTR properties. The Foreign Investment Review Board (FIRB) approval process has been streamlined for passive institutional investors who demonstrate a "strong track record of compliance".1 Critically, application fees for BTR developments have been significantly reduced by applying "commercial land" fees instead of the substantially higher "residential land" fees. For example, a A$40 million land acquisition for a BTR project would see the FIRB fee reduced from approximately A$1.1 million to a mere A$14,000, effectively removing a major financial barrier for foreign capital.1

Federal BTR Tax Concessions (BTR Bill, passed November/December 2024): The passage of this legislation introduced two key federal tax incentives. Firstly, the capital works deduction rate has increased from 2.5% to 4% per year for eligible new BTR developments, effectively cutting the depreciation period from 40 years to 25 years.1 Secondly, the final withholding tax rate on "eligible fund payments" and capital gains from Managed Investment Trust (MIT) investments for eligible BTR developments has been reduced from 30% to 15%, effective July 1, 2024.1 This aligns BTR investments with the taxation rate of other commercial property investment options, making them more competitive.24 Furthermore, the 15-year limit on BTR tax concessions has been removed, meaning accelerated capital works deduction and withholding tax concessions continue as long as the single ownership criterion and other eligibility criteria are met.1 The scope of eligible fund payments has also been expanded to include capital gains on the disposal of a BTR dwelling and capital gains on the disposal of membership interests in an entity referable to an eligible BTR development, providing crucial clarity on tax implications for exit strategies.1

State BTR Tax Concessions: Beyond federal measures, most Australian jurisdictions have introduced additional concessions to facilitate BTR investment. These typically include significant land tax reductions (e.g., a 50% reduction in land value for land tax calculation in New South Wales, Victoria, Queensland, Western Australia, and South Australia) and exemptions or refunds of surcharge purchaser duty and land tax.1

Sustainability and Tenant-Friendly Features: The long-term ownership model inherent in BTR developments provides strong financial incentives for building owners to design and construct better quality, more sustainable housing. This focus on energy efficiency, environmental performance, and tenant comfort not only aligns with modern investment mandates but also effectively attracts and retains quality tenants, contributing directly to long-term asset value and reduced operational costs.24

Australia's BTR sector historically faced significant regulatory hurdles, including a lack of competitive tax incentives and a laborious FIRB approval process, which made it less attractive for international institutional capital.1 The comprehensive suite of federal and state tax concessions, coupled with the streamlining of FIRB approvals and fee reductions1, directly addresses these long-standing barriers. The reduction in the MIT withholding tax rate from 30% to 15% is particularly crucial for attracting foreign capital, as it makes Australian BTR more competitive on a global scale.29 These targeted incentives act as a powerful de-risking mechanism for foreign investors, significantly improving the financial viability and competitiveness of Australian BTR projects compared to other asset classes or un-incentivized residential developments. The removal of the 15-year limit on certain tax concessions further enhances investment certainty and maintains asset value for subsequent investors1, signaling a long-term commitment from the government. This also suggests that the government is actively working to level the playing field for institutional investors, addressing historical disadvantages compared to individual landlords.16

2.4 Risks and Challenges

Despite the compelling benefits, investing in the Australian BTR sector is not without its risks and challenges:

Nascent Market Stage and GST Leakage: The BTR industry in Australia is still in its early stages of development. It represents only 0.2% of the residential housing market, which is significantly smaller when compared to the 12% penetration in the US and 5.4% in the UK.1 A major financial obstacle for BTR developers is their current inability to claim Goods and Services Tax (GST) credits on related expenses such as land acquisition, construction, and other development costs. This results in a persistent 10% GST leakage, which directly impacts project feasibility and returns.1 Currently, there are no proposals to introduce GST concessions or exemptions specifically for BTR projects.1

Regulatory Uncertainty and Tiered Trust Structure Restrictions (BTR Bill): While the BTR Bill has passed2, its legislative journey faced initial uncertainty.1 A critical restriction within the BTR Bill is that access to the 15% withholding concessions is limited where eligible fund payments flow through a tiered trust structure, unless the Managed Investment Trust (MIT), intermediary trusts, and the BTR development owner have the same trustee.1 This requirement significantly narrows the class of investors for whom the concessions are available, potentially limiting broader institutional participation, particularly for complex fund structures common in international real estate investment.1

Affordable Housing Requirements and Impact on Returns: A key eligibility criterion for federal BTR tax concessions is the requirement for 10% of dwellings within a development to be offered as "affordable tenancies." These are defined as units rented for 74.9% or less of the market rent for comparable dwellings.1 This affordable housing component can erode more than half the financial advantage gained from lowering the MIT tax concessions to 15%, potentially deterring some BTR investors if the perceived net return on investment is not as lucrative as initially modeled, especially when compared to alternative investment opportunities.1

Insufficiently Concessional Bills and Withholding Tax Disparity: The BTR Bills, in their current form, are not universally considered sufficiently concessional to achieve the desired level of impact and attract the full scale of foreign institutional capital.1 If the eligibility criteria remain onerous and the concessions are not more financially attractive, foreign capital may continue to favor more established BTR markets like the US and UK, where there is less perceived risk associated with return on investment and potentially more favorable tax regimes.1 Furthermore, while the proposed 15% withholding tax rate aligns BTR with some commercial property assets, it is still higher than for other asset classes, such as certified "clean buildings," which are eligible for a more favorable 10% rate.1

Lack of Retrospective Application: A significant concern for early market participants is that the current form of the Bills prejudicially affects investors who commenced capital works prior to May 9, 2023, as they cannot access the full suite of concessions. This could create an uneven playing field between new and existing BTR assets and potentially lead to "stranded" ineligible BTR assets that are less competitive or profitable.1

State-Specific Eligibility Criteria: Investors must navigate varying and complex state-specific eligibility criteria for BTR tax concessions, adding a layer of administrative burden and complexity. For instance, New South Wales has a labor force hour requirement for construction, and Western Australia has specific occupancy dates and continuous qualification periods that must be met to qualify for state-level benefits.1 Moreover, Tasmania, the Northern Territory, and the Australian Capital Territory have not yet introduced any BTR concessions, creating a fragmented regulatory landscape across the country.1

While government incentives are clearly a significant benefit, a deeper review of the BTR Bill's specifics reveals critical limitations. The restriction on tiered trust structures1 is particularly problematic for common institutional investment vehicles, and the affordable housing requirement1 directly impacts the net financial benefit. These "onerous conditions"29 are explicitly cited as potential deterrents to foreign capital1, suggesting a tension between policy goals (increasing supply, promoting affordability) and investor appetite. This indicates that the policy, while well-intentioned, may inadvertently create a "two-speed" market or fail to attract the desired scale of foreign institutional investment if the perceived net benefits are insufficient compared to alternative global opportunities. European private credit funds must conduct exceptionally thorough due diligence on the specific project's eligibility for these concessions and the implications of its ownership structure to ensure the intended tax benefits are fully realizable. This also highlights a potential area for ongoing industry lobbying to refine these policies for broader effectiveness.

2.5 Operational Considerations and Best Practices

For BTR developments, achieving optimal operational and cost efficiency is paramount, given their long-term ownership model.25 Professional property management is critical for achieving high tenant retention rates and minimizing operational costs, which directly impacts income stability and overall asset performance.1

Key operational strategies include fostering a strong sense of community among tenants through planned events and shared amenities, proactively addressing maintenance and repairs in a timely manner, and establishing efficient vendor relationships. These practices are essential for reducing high tenant turnover, which can significantly diminish income.25 To maintain appeal and viability during economic fluctuations, implementing flexible leasing options and offering promotional pricing can attract renters, especially when consumer income and affordability are under pressure.31

The adoption of digital tools and smart technology is increasingly vital for various aspects of property management. Automated rent collection, streamlined maintenance request systems, and advanced analytics platforms can significantly improve the tenant experience, cut administrative time, and reduce overall operational costs.32 These technologies not only enhance efficiency but also provide valuable data for optimizing building performance and CapEx decisions.33

The core BTR model is predicated on professional landlordism and long-term tenant relationships, fundamentally differing from traditional build-to-sell or small-scale private rentals.1 High tenant turnover is explicitly identified as a factor that "reduce[s] income".25 Therefore, effective property management, proactive maintenance, and strategic community building are not merely administrative functions but direct drivers of financial performance and asset value.31 For private credit funds, assessing the operational capabilities and track record of the BTR developer/manager is as critical as evaluating the financial projections. Lenders should scrutinize operational plans, tenant retention strategies, and the integration of technology to ensure the project can achieve and maintain high utilization rates, minimize operational costs, and ultimately safeguard debt service coverage. This also suggests that projects with strong Environmental, Social, and Governance (ESG) practices, particularly in sustainable building and tenant well-being, may offer lower long-term operational risks, higher tenant appeal, and potentially access to green financing, further enhancing their investment profile.24

3. Australian Purpose-Built Student Accommodation (PBSA) Sector Analysis

3.1 Definition and Core Characteristics

Purpose-Built Student Accommodation (PBSA) refers to buildings specifically constructed and professionally managed to provide sleeping and living facilities primarily for university students.34 These developments are distinct from traditional residential housing. It is important to note that PBSA buildings are often classified as non-residential building jobs by the Australian Bureau of Statistics (ABS) because they typically do not meet the definition of a residential building (i.e., intended for long-term use with cooking and bathing facilities in each unit) under the Functional Classification of Buildings (FCB). This classification presents a challenge in directly estimating the sector's market size from standard residential building approvals data, as PBSA values contribute to a broader non-residential series.34

PBSA offerings typically include a mix of fully self-contained units and rooms with shared facilities, such as communal kitchens or living areas. These are frequently complemented by a range of on-site amenities like study spaces, gyms, and social areas, fostering a structured community environment.3 Professional management is a hallmark of the PBSA sector, contributing significantly to the safety, security, and overall community experience for students, which serves as a key differentiator from the broader, often less regulated, private rental market.3

3.2 Market Size and Growth Forecasts

The Australian PBSA sector has demonstrated consistent growth in recent years. Between the 2021/22 and 2023/24 financial years, a total of 9,759 student accommodation rooms were approved for construction across Australia.34 Approvals have shown a steady and accelerating growth trend: 1,684 rooms were approved in 2021/22, increasing to 2,897 rooms in 2022/23, and then jumping significantly to 5,178 rooms in 2023/24.34

Geographically, New South Wales (NSW) led in approvals during this period with 4,791 rooms, accounting for 49.1% of the total. Victoria followed with 1,735 rooms (17.8%), and Western Australia with 1,706 rooms (17.5%). Key local government areas (LGAs) for approvals include Randwick and City of Sydney in NSW, and City of Melbourne in Victoria.34

As of Semester 1 2025, the top 16 private sector managers collectively control 61,785 operational beds, with an additional pipeline of 14,581 beds across 27 planned properties, indicating a strong appetite for increasing exposure to Australian student accommodation.6 Overall, there are approximately 100,000 PBSA beds across Australia, with a further 35,605 beds in the development pipeline.23 Currently, 16 PBSA projects are under construction across Australia's capital cities, totaling over 8,700 beds, representing the largest number of new student accommodation projects under construction since the COVID-19 pandemic.6 Over the next three-year cycle, more than 12,000 new student accommodation beds are projected to be added, with Sydney (4,300 beds) and Brisbane (over 3,160 beds) expected to be standout performers. While Melbourne's pipeline has temporarily slowed, it is anticipated to recover with 1,500 new beds by 2027.6

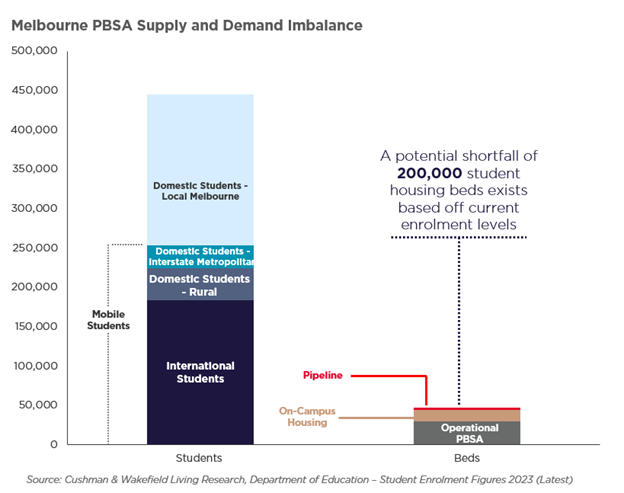

Despite the observed growth in PBSA approvals and pipeline6, multiple sources consistently highlight a severe "pressing shortage of purpose-built accommodations"4 and a "significant gap" between potential demand and current supply.3 Cushman & Wakefield's research estimates a substantial potential shortfall of 200,000 appropriate student housing beds based on 2023 enrolment levels.3 Even with projects underway, the supply "still fall[s] short of the projected future demand".4 This persistent and significant undersupply is the most fundamental and compelling driver of investment opportunity in the PBSA sector. It strongly indicates that the market can absorb new supply, leading to sustained high occupancy rates and robust rental growth, even as new developments come online. For private credit funds, this structural imbalance translates into lower default risk on loans due to strong underlying asset performance and consistent tenant demand, making it a highly attractive sector for debt financing. The market is far from saturated, offering ample room for new, well-located developments.

Table 2: Australian PBSA Market Supply and Demand

| Metric | Value/Status | Source |

|---|---|---|

| Total Operational Beds (Overall) | ~100,000 | 23 |

| Operational Beds (Top 16 Managers, S1 2025) | 61,785 | 6 |

| Beds Under Construction (Overall) | 6,912 - 8,700 | 6 |

| Beds in Development Pipeline (Overall) | 35,605 | 23 |

| Annual Approvals (FY 2021/22) | 1,684 rooms | 34 |

| Annual Approvals (FY 2022/23) | 2,897 rooms | 34 |

| Annual Approvals (FY 2023/24) | 5,178 rooms | 34 |

| Projected New Beds (next 3-year cycle) | 12,000 | 6 |

| Estimated Bed Shortfall (2023 enrolments) | 200,000 | 3 |

| Students per PBSA bed (Melbourne) | 8.67 | 3 |

| Students per PBSA bed (National Average) | 7.27 | 3 |

| International Student Enrolments (2022) | 300,000 | 21 |

| International Student Enrolments (2023) | 560,000 | 21 |

| International Student Enrolment Increase (Uni Melbourne 2024) | 12% | 3 |

| International Student Enrolment Increase (RMIT 2024) | 17% | 3 |

Note: Data points are sourced from various reports and may reflect different reporting periods within the specified years.

3.3 Demand Drivers: International and Domestic Student Growth

The demand for PBSA in Australia is propelled by a dual engine of international and domestic student growth.

International Students: Education exports represent a substantial pillar of the Australian economy, contributing approximately $50 billion in 2023/24 and ranking as the nation's fourth-largest export category.21 Following the disruptions of the COVID-19 pandemic, international student numbers have rebounded sharply, increasing from just under 300,000 in 2022 to 560,000 by the end of 2023.21 Melbourne, in particular, maintains a strong global reputation as a premier destination for international students, consistently ranking high (5th globally in 2025) as a "best student city".3 The city accounts for a substantial 42% of Australia's national PBSA bed supply and exhibits a high ratio of 8.67 students per PBSA bed, well above the national average of 7.27, underscoring concentrated demand.3 Leading universities within Melbourne, such as the University of Melbourne and RMIT, reported significant increases in international enrolments in 2024 (12% and 17% uplift, respectively), demonstrating continued momentum despite proposed policy measures to curb numbers.3 China (23%) and India (17%) remain the largest source countries for international students21, with the rapid growth of India's middle class expected to drive continued upward trends in demand from this region.4 Students, particularly international ones, consistently express a preference for purpose-built accommodation due to its perceived safety, comprehensive amenities, and supportive community environment, further solidifying the demand for PBSA.3

Domestic Students: Beyond the international cohort, there is a notable and increasing trend of domestic students relocating for study. Nearly 20% of Australian students were enrolled in universities outside their home state in 2023, a significant rise from under 10% in 2009.3 These domestic students are increasingly considering PBSA as a viable housing option, largely driven by the mounting pressures and affordability challenges prevalent in the broader private rental market.3

While international students have historically been, and continue to be, the primary demand driver for PBSA3, the research highlights a significant and growing trend of domestic students seeking PBSA options due to the broader pressures in the private rental market.3 This indicates a broadening of the demand base beyond a single cohort. This diversification of the tenant base adds a crucial layer of resilience to the PBSA sector, making it less susceptible to potential shocks or policy-induced fluctuations specifically targeting international student numbers. For investors, a diversified demand profile reduces risk and enhances the long-term stability and predictability of income streams, making PBSA a more robust and attractive investment proposition. It suggests that even if international student numbers face headwinds, domestic demand could provide a significant buffer.

3.4 Key Benefits for Investors

Investing in Australian PBSA offers several distinct advantages for private credit funds:

Strong Occupancy and Rental Growth: Major PBSA operators, such as Scape in Melbourne, report "solid leasing velocity and consistent rental growth year on year across the Melbourne portfolio," indicative of a healthy and profitable market.3 Knight Frank data further illustrates this trend, showing sharp increases in PBSA rental rates since 2018, with studio apartments in Sydney experiencing a 50% increase and Melbourne a 38% increase.35 This robust performance underscores the strong demand and limited supply dynamics within the sector.

Resilience and Diversification: The PBSA sector demonstrated a quicker-than-anticipated recovery following the COVID-19 pandemic, with strong rental growth observed throughout 2023.4 This resilience highlights its capacity to withstand economic shocks and recover swiftly. Investing in PBSA also offers valuable portfolio diversification, providing an alternative asset class with potentially lower correlation to traditional real estate or public market fluctuations, thereby enhancing overall portfolio stability.17

Alleviating Broader Rental Market Pressure: PBSA plays a crucial role in the wider housing ecosystem by providing dedicated, student-only housing options. This directly alleviates pressure on the mainstream private rental market, freeing up dwellings that would otherwise be occupied by students for other demographics, such as families and essential workers.3 For example, the addition of 3,000 new PBSA beds in Melbourne could theoretically free up approximately 950 dwellings in the inner-city market, demonstrating its significant contribution to broader housing solutions.3 This positions PBSA not merely as student infrastructure but as a critical component of the urban housing mix.3

Government Support and Recognition: The federal government has explicitly linked increased international student intake to universities demonstrating their commitment to providing additional student housing.5 This policy signals a clear and growing governmental push for more PBSA development, recognizing its importance in both education and housing policy. Industry bodies like the Student Accommodation Council (SAC) are actively advocating for the removal of barriers to growth, such as foreign investor taxes and charges, and for consistent regulatory frameworks, further indicating a supportive environment for the sector.5

The research explicitly frames PBSA as "not merely as student infrastructure, but as a critical component of Melbourne's urban housing mix".3 The ability of PBSA to "free up around 950 dwellings for families, essential workers, and the wider population"3 underscores its broader societal benefit beyond just accommodating students. Policymakers are actively urged to "remove barriers to planning approvals, enabling institutional investment, and supporting long-term development pipelines"3 for PBSA, recognizing its contribution to livability and competitiveness. This strong articulation of PBSA's role in addressing the wider housing crisis positions it as a politically supported and socially beneficial asset class. For investors, this translates into a higher likelihood of continued government backing, potentially leading to smoother planning approvals, reduced regulatory hurdles, and even future incentives. It suggests that investments in PBSA align with broader public policy goals, which can offer a valuable "social license to operate" and enhance long-term stability for institutional investors.

3.5 Risks and Challenges

Despite its strong demand drivers, the Australian PBSA sector faces several risks and challenges:

Significant Supply Shortfall and Slow Development Velocity: Despite Melbourne being Australia's largest PBSA market, there remains a substantial gap between potential demand and current supply.3 Melbourne's development velocity is notably slow, with its pipeline representing only 8.2% of existing operational stock, significantly less than Sydney's 18.6%.3 The estimated national shortfall of 200,000 beds highlights the immense scale of this supply challenge, indicating that new developments, while increasing, are still not keeping pace with demand.3

Construction and Operational Cost Pressures: Addressing the existing supply shortage is complex, primarily due to elevated construction and labor costs, persistent difficulties in obtaining planning approvals, and limited availability of suitable land in key urban centers.4 Furthermore, operational costs (OPEX) have been rising significantly, with the average cost per bed increasing by 23% annually since 2022, largely driven by higher statutory costs. These rising costs directly impact the feasibility and profitability of new PBSA projects.6

Impact of Policy Measures on International Student Enrolments: While early indicators for 2024 show continued momentum in international enrolments, the sector is sensitive to government policy. The article notes "headlines and various proposed policy measures to curb international student enrolments over the past 18-months"3, which could potentially impact future demand. Student visa grants have, in fact, fallen since mid-2023, particularly for Vocational Education and Training (VET) students, indicating a tightening in government approach to migration.21

The Australian government's approach to international student numbers presents a complex dynamic for the PBSA sector. On one hand, there is clear recognition of the need for more student housing, with policies linking increased university student intake to the provision of new accommodation.5 This signals a desire to support the sector's growth. However, this ambition is juxtaposed with simultaneous policy measures and public discourse aimed at curbing overall international student enrolments, driven by concerns over population growth and housing affordability.3 This creates a tension between the government's desire to increase housing supply through PBSA and its efforts to manage migration numbers. For investors, this means that while the fundamental demand for student accommodation remains strong due to the existing undersupply, the future trajectory of student enrolments, particularly international ones, requires careful monitoring of policy implementation and its actual impact on demand. The sector's viability depends on a delicate balance between these competing policy objectives.

3.6 Operational Considerations and Best Practices

For PBSA, professional management is crucial not only for day-to-day operations but also for enhancing the student experience, ensuring high retention rates, and ultimately preserving asset value.3 Given the unique needs of a student cohort, operational strategies must be tailored to foster a supportive and engaging living environment.

Key operational strategies include proactive community integration and promoting social interaction among residents, which are vital for student well-being and academic success.38 Addressing the diverse needs of students, particularly regarding affordability and accessibility, is also paramount, as PBSA can be expensive and limited for low-income students.38

Leveraging technology is increasingly important for operational efficiency and enhancing the tenant experience. This includes implementing AI-driven housing allocation systems, blockchain-based rental agreements, and flexible leasing models to improve accessibility and streamline processes.38 Digital tools for maintenance requests, automated booking systems, and advanced analytics platforms can also significantly cut administrative time, reduce operational costs, and provide real-time insights into building performance and tenant behavior.32 These technological advancements not only improve efficiency but also contribute to a competitive advantage in attracting and retaining students.

The unique characteristics of the student demographic necessitate tailored operational strategies. Unlike general residential tenants, students, particularly international ones, often seek a comprehensive living experience that extends beyond just a room. This includes a strong sense of community, safety, and access to specific amenities.3 Therefore, operational strategies must prioritize community building, student well-being, and seamless service delivery. The effective integration of technology, from automated processes to data analytics, can provide a competitive advantage by enhancing the student experience while simultaneously optimizing cost management and operational efficiency.32 For investors, this means that the operational expertise of the PBSA manager is a critical factor in ensuring stable returns and long-term asset value. Projects that demonstrate a strong commitment to these tailored management practices are likely to achieve higher occupancy rates and better rental growth, thereby de-risking the investment.

4. Macroeconomic and Government Support Landscape

4.1 Australian Economic Outlook (GDP, Inflation, Employment)

Understanding the broader Australian economic landscape is crucial for assessing the viability of BTR and PBSA investments.

GDP Growth: Australia's economic momentum slowed in early 2025, with Gross Domestic Product (GDP) rising just 0.2% in the March quarter, a notable drop from the 0.6% growth recorded at the end of 2024. This slowdown was partly attributed to a sharp pullback in public spending. Forecasts for real GDP growth indicate a moderate trajectory: 1.0%-1.2% in 2024, an expected increase to 1.6%-1.8% in 2025, and further growth to 2.0%-2.1% in 2026.40 The Reserve Bank of Australia (RBA) has slightly lowered its outlook for productivity growth, contributing to these revised GDP forecasts.41

Inflation: Headline Consumer Price Index (CPI) fell to 2.1% in May 2025, with trimmed mean inflation easing to 2.4%.40 The RBA forecasts underlying inflation to be around 2.7% by June 2027, within its target range.42 However, some volatility in headline inflation is expected over 2025-2026 due to the unwinding of electricity rebates.41

Employment: The Australian labour market remains resilient, but job growth is anticipated to slow.40 The unemployment rate climbed from 4.1% to 4.3% in June 2025, a sign that the labour market is beginning to soften.43 The RBA expects unemployment to remain steady at 4.3% through 2027.44 Despite this, total employment in Australia is projected to grow significantly, by approximately 6.6% (or 950,000 people) over the next five years, and by nearly 13.7% (or 2 million people) over the next decade, reaching 16.3 million employed people by May 2034.45

Impact on Rental and Student Accommodation Demand: Long-term housing demand in Australia is largely a function of population growth and household formation.18 Population growth, particularly driven by net overseas migration of working-age adults, immediately adds to housing demand.20 The population growth rate rebounded to 2.5% per annum in mid-2023 after border reopenings.19 This strong demand, coupled with housing supply not keeping pace, has led to rapid rental price growth and historically low national vacancy rates, hovering around 1% in 2023.15 While international students contribute to overall demand, their direct impact on overall private rental prices is considered marginal, estimated at around a 0.5% increase for every 100,000 additional students.36 Instead, the broader imbalance between new supply and new demand, exacerbated by rising interest rates that have increased mortgage repayments and pushed more households into the rental market, is a key factor driving rental pressures.19

While Australia's GDP growth is moderating and inflation is easing, the underlying housing market dynamics, particularly in the rental sector, remain driven by structural factors like population growth (especially net overseas migration of working-age adults) and persistent undersupply.16 The RBA notes that international students, while contributing to demand, are not the primary driver of the rental crisis.36 Instead, the imbalance between new supply and demand, exacerbated by rising interest rates impacting mortgage holders and pushing more people into the rental market, is the key factor.19 This suggests that even in a period of slower economic growth and easing inflation, the fundamental demand for rental accommodation, including BTR and PBSA, will likely remain robust due to deep-seated structural issues in housing supply and demographic shifts. For private credit funds, this means that while broader economic conditions might influence borrower capacity, the underlying asset performance (occupancy, rental growth) in these sectors is likely to be resilient, providing a degree of insulation from macro fluctuations.

4.2 Government Policy and Support

The Australian government, at both federal and state levels, is actively implementing policies and providing support to stimulate investment in BTR and PBSA, recognizing their critical role in addressing the national housing shortage.

BTR Specific Incentives:

Federal Support: The federal government has introduced significant tax incentives for eligible new BTR developments. This includes a reduction of the Managed Investment Trust (MIT) withholding tax rate from 30% to 15% and an increase in the capital works deduction rate from 2.5% to 4% per year. These measures apply to developments that become operational after July 1, 2023, and before June 30, 2030, provided they offer at least 10% of their dwellings as affordable housing (rented at 74.9% or less of market rent).1

FIRB Reforms: The Foreign Investment Review Board (FIRB) approval process has been streamlined for BTR investments. This includes allowing foreign investors to purchase established BTR properties (conditional on continued BTR operation) and significantly reducing FIRB application fees by applying commercial land fee tiers instead of the higher residential land fees.1

State-Level Concessions: Most Australian states have introduced their own BTR tax concessions. These typically include substantial land tax reductions (e.g., a 50% reduction in land value for land tax calculation in New South Wales, Victoria, Queensland, Western Australia, and South Australia) and exemptions or refunds of surcharge purchaser duty and land tax.1

BTR Misuse Tax: To ensure the integrity of these concessions, the Capital Works (Build to Rent Misuse Tax) Bill 2024 introduces a clawback mechanism. This BTR Misuse Tax is designed to recover tax benefits claimed by BTR owners if their developments cease to qualify as Active BTR Development during a 15-year compliance period.1

PBSA Specific Incentives:

Federal Policy Linkage: The federal government has explicitly linked increased international student placements to universities demonstrating their commitment to providing additional student housing. The cap for international student places has been lifted by 25,000 to 295,000 for 2026, but this increase comes with a condition: public universities must prove they are creating enough housing to support both domestic and international students if they wish to increase their intake.5 This policy actively encourages collaboration between universities and the private PBSA sector to meet housing demand.

Industry Advocacy: Industry bodies such as the Student Accommodation Council (SAC) are actively advocating for further government support. Their priorities include recognizing PBSA as a "priority asset class," removing foreign investor taxes and charges, ensuring consistent regulatory frameworks across jurisdictions, and establishing accelerated development pathways to increase the supply of new student housing.5

State-Level Planning Support: Western Australia, for instance, has released a draft Position Statement on Purpose-Built Student Accommodation. This aims to provide clear guidance on design considerations and address key planning aspects for PBSA developments, recognizing its role in enhancing student experience, boosting the local economy, and contributing to broader housing affordability solutions.48

The Australian government, at both federal and state levels, is increasingly recognizing the critical role of institutional investment in BTR and PBSA to address the national housing crisis.1 The specific tax concessions, FIRB reforms for BTR, and the direct linkage of university student intake to housing provision for PBSA1 demonstrate a deliberate policy shift to incentivize large-scale, professionally managed rental supply. This is a departure from a historically fragmented private rental market.22 This alignment of government policy with the objectives of institutional investors creates a more supportive and predictable operating environment. It suggests that future policy decisions are likely to continue favoring these sectors, potentially leading to further de-risking of investments through continued regulatory support, streamlined processes, and a shared interest in increasing housing supply. For private credit funds, this means a more stable regulatory backdrop, reducing the risk of adverse policy changes and enhancing the long-term viability of their lending facilities.

5. Financial Considerations for European Private Credit Funds

5.1 Direct Lending Facilities in Australian Real Estate

Market Trends: Australia's private credit market is rapidly growing in importance for real estate financing. CBRE forecasts the size of private credit-funded real estate debt to increase significantly from $50 billion currently to $90 billion by 2029.10 This segment already accounts for a substantial 26% of residential development debt and 4.2% of commercial property debt.10

Why Private Credit: The expansion of private credit in Australia is largely a response to the retreat of major banks from certain real estate lending segments. This retrenchment by traditional lenders is a consequence of increased regulations and higher capital requirements implemented following the Global Financial Crisis.10 Private credit funds offer a flexible and swift alternative, providing customized solutions that may not be available through traditional banking channels. For borrowers, private credit can also offer access to new capital without diluting existing ownership stakes, a key advantage over equity financing.17

Typical Terms & Collateral: Direct lending facilities in Australian real estate are typically secured by tangible property, providing a built-in equity buffer that is crucial for capital preservation in the event of borrower default, as the property can be sold to recover investor capital.10 These funds often target returns in the range of 7% to 11% per annum, offering a material premium over traditional term deposits and government bonds.10 Loans commonly feature floating coupon rates, which can provide a hedge against inflation.49 While traditional bank loans may stretch over 5-7 years, private credit typically operates on shorter durations, often between 1-3 years.50 Loan-to-value ratios (LVRs) for residential development and property investment segments are generally around 65%, though for higher-risk assets like land banks or pre-development sites, LVRs can be lower (50-65%).51 Some non-bank lenders maintain a conservative maximum LVR of 75%.52 Loan agreements typically include financial covenants (e.g., interest cover ratios, leverage ceilings) and regular reporting requirements (monthly or quarterly), which can sometimes be more stringent than those imposed by banks.50 Borrowers may also face exit or early repayment penalties and, in some cases, private credit deals may include potential equity components such as warrants or convertible notes.50

Due Diligence Process: A thorough due diligence process is paramount for private credit lenders. This involves a comprehensive investigation of the potential borrower's creditworthiness and risk level, as well as detailed searches relating to the property offered as security.52 Key aspects of due diligence include:

- Background Checks: Conducting credit checks, online searches for negative mentions, and legal database reviews on the borrower and any guarantors to assess their financial soundness and history.52

- Property Valuation: Ensuring the property's value is sufficient to cover the loan in case of default. This is typically determined by a combination of online valuations, in-person appraisals by local real estate agents, and/or sworn valuation reports.52 Lenders typically require a lower LVR to provide a buffer against market fluctuations.52

- Repayment and Exit Strategy Assessment: Scrutinizing the borrower's plan to repay the loan, whether through refinancing with a bank or property sale. This involves verifying the feasibility of the exit strategy with brokers and assessing the realism of listing prices for properties to be sold.52

BTR Specifics: For BTR projects, lenders assess risks across four distinct phases: land acquisition and early works, construction, pre-leasing and launch, and operation and occupation.54 Risk mitigants during the construction phase include loan-to-value and loan-to-cost covenants, quantity surveyor reports, assessment of builder expertise, and various tripartite deeds and undertakings to manage cost overruns.54 For the operational phase, conditions for funding transition often include evidence of practical completion, achievement of pre-leasing targets, acceptable "as complete" valuations, and compliance with new operational financial covenants.54

Role of Australian Partner Firms: For European private credit funds, an Australia-based partner firm is critical for successful direct lending in the real estate sector. These partners provide essential local market expertise, facilitating deal origination and navigating the specific regulatory nuances of the Australian market.11 They offer specialized credit expertise in real estate development.49 Furthermore, local partners are crucial for conducting robust customer due diligence, which can be particularly challenging for foreign non-bank lenders due to a relatively low rate of direct customer interaction and a reliance on brokers.57 The partner's role extends to assessing governance structures, valuation practices, and investor protection measures, especially given the Australian Securities and Investments Commission's (ASIC) increased scrutiny of private credit funds.58

Australia's private credit market is rapidly expanding, filling the void left by traditional banks in certain real estate segments.10 However, this growth is accompanied by increased regulatory scrutiny from bodies like ASIC58, and inherent complexities such as the reliance on brokers for customer interaction in non-bank lending.57 The market also lacks a central source for pricing data or covenant benchmarks.50 For European private credit funds, a robust Australian partner firm is not merely a facilitator but a strategic imperative. This partner's deep local market knowledge, established networks for deal origination, and expertise in navigating the evolving regulatory landscape (including due diligence and compliance) are essential to mitigate risks and unlock opportunities. The partner acts as a critical bridge, providing transparency and expertise that is otherwise difficult to obtain in a less standardized, yet rapidly growing, private credit ecosystem. This local expertise ensures that direct lending facilities are structured appropriately, risks are accurately assessed, and the investment is protected.

5.2 Foreign Exchange and Interest Rate Differentials

For European private credit funds, understanding and managing foreign exchange (FX) and interest rate differentials between Australia and the Eurozone is critical for preserving investment returns.

AUD/EUR Exchange Rate Dynamics: The Australian dollar (AUD) is historically considered a 'risk currency' relative to the US dollar, meaning it tends to depreciate in response to negative shifts in global risk sentiment and vice versa.12 The Reserve Bank of Australia's (RBA) monetary policy decisions play a key role in influencing the exchange rate. An increase in Australian interest rates relative to those in Europe would typically increase demand for the AUD, leading to its appreciation, and conversely, a decline in Australian rates would lead to depreciation.7 The EUR/AUD currency pair has recently been observed in a bullish flag pattern, suggesting a potential continuation of its upward trend.8

Interest Rate Differentials (Australia vs. Eurozone):

- Australia's Cash Rate: The RBA has been in an easing cycle. The cash rate was cut to 3.60% in August 2025, with economists at CBA expecting another cut to 3.35% in November 2025.44 The RBA's own forecasts are underpinned by an assumption of further rate cuts, bringing the cash rate below 3% in the current cycle, with a long-term projection around 2.85% in 2026.8

- Euro Area Interest Rate: The European Central Bank (ECB) has paused its easing cycle, with the main refinancing operations rate at 2.15% as of July 2025, after eight cuts over the past year.60 Market consensus suggests modest rate cuts may resume in mid-to-late 2025, potentially bringing the deposit rate closer to 3.0% by the end of 2026, or even 1.75%-2.00% by year-end 2025 according to Morningstar.61 The long-term projection for the Euro Area interest rate is around 2.15% in 2026 and 2.40% in 2027.60

Implications for Yield and Arbitrage: Interest rate differentials are a key driver of international capital flows and exchange rates.7 While theoretical arbitrage opportunities arising from interest rate differentials are typically short-lived and quickly exploited by sophisticated trading programs62, FX forward curves are constructed precisely to eliminate such risk-free arbitrage, ensuring that there is no inherent advantage to holding one currency over another solely due to interest rate differences.63 For a European investor, if Australian interest rates are higher than Eurozone rates, Australian assets become more attractive, increasing demand for the AUD.7 However, if the Euro (EUR) is the lower yielding currency, hedging the AUD exposure back to EUR will likely incur a cost, as the forward rate will be less favorable than the current spot rate.63

Currency Hedging Strategies: Currency hedging aims to minimize the impact of foreign currency movements on the underlying investment returns, thereby reducing volatility and mitigating unintended currency bets.12 For European investors, this means implementing strategies to protect their EUR-denominated returns from adverse AUD/EUR fluctuations.12 Common hedging instruments include forward contracts, which allow investors to lock in an exchange rate for a future date, providing certainty on costs for future payments or repatriated income.13 Additionally, natural hedging strategies can be employed, such as netting foreign currency receivables against payables, incorporating currency clauses in contracts, or strategically timing payments (leading or lagging) to balance currency exposures and reduce overall transaction costs.65 A combination of natural hedging techniques and financial derivatives can be utilized to fine-tune currency protection for remaining exposures.65

The Australian and Eurozone economies are on different monetary policy paths, with Australia's RBA still in an easing cycle and the ECB pausing after cuts.44 While theoretical arbitrage opportunities from interest rate differentials are quickly closed by market mechanisms62, these differentials directly influence capital flows and the AUD/EUR exchange rate.7 For European investors, a higher-yielding AUD environment means that hedging back to EUR will likely incur a cost, as the forward rate will be less favorable than the spot rate.63 This necessitates a proactive and sophisticated currency risk management strategy for European private credit funds. Relying solely on the underlying asset's performance without considering FX exposure could significantly erode EUR-denominated returns. Implementing a tailored hedging program, potentially combining financial instruments like forward contracts with operational hedging techniques, is crucial for preserving the intended yield and managing portfolio volatility. The choice of hedging strategy should be carefully considered based on the fund's risk appetite, time horizon, and the expected trajectory of interest rate differentials.

6. Conclusions and Recommendations

The Australian Build-to-Rent (BTR) and Purpose-Built Student Accommodation (PBSA) sectors present a compelling, albeit evolving, investment landscape for European private credit funds. The underlying structural housing supply deficit, robust demographic growth, and increasing governmental support create a strong fundamental demand for these asset classes. Both sectors offer the potential for stable, long-term, and inflation-linked income streams, aligning well with the objectives of private credit investors.

The BTR sector, despite its nascent stage, is experiencing significant acceleration driven by recent federal and state tax concessions and streamlined foreign investment processes. These policy shifts are actively de-risking the sector for institutional capital, making it more competitive on a global scale. However, challenges such as GST leakage, restrictions on tiered trust structures for tax concessions, and the impact of affordable housing requirements necessitate meticulous due diligence on project-specific eligibility and financial modeling.

The PBSA sector benefits from a strong and diversifying demand base, fueled by both rebounding international student enrolments and increasing domestic student mobility. Its role in alleviating pressure on the broader rental market positions it as a socially and politically supported asset class, potentially leading to smoother planning approvals and sustained government backing. Nevertheless, the substantial supply shortfall and rising construction and operational costs remain key challenges, alongside the need to monitor potential policy shifts affecting student migration.

The Australian private credit market is growing rapidly, offering a flexible and efficient financing avenue for these real estate sectors, particularly as traditional banks retrench. However, the market's less standardized nature and increased regulatory scrutiny underscore the critical importance of local expertise. Managing foreign exchange and interest rate differentials is paramount; while direct arbitrage opportunities are fleeting, the cost of hedging AUD exposure back to EUR will directly impact net returns and requires a sophisticated risk management approach.

Strategic Considerations for European Private Credit Funds:

Direct Lending Facilities: The growing Australian private credit market could serve as a mechanism for access to these sectors. This allows for customized deal structures and fills the funding gap left by traditional banks in the BTR and PBSA sectors.

Local Partnership Considerations: Establishing relationships with experienced Australia-based partner firms could provide value through:

- Deal Origination: Identifying BTR and PBSA projects with strong fundamentals and alignment with government incentives.

- Due Diligence: Conducting assessments of borrower creditworthiness, property valuations, and the operational capabilities and track record of BTR/PBSA managers, including tenant retention strategies, community building initiatives, and technology integration.

- Regulatory Navigation: Navigating the complex federal and state tax concessions, FIRB requirements, and other regulatory nuances, particularly concerning tiered trust structures and affordable housing mandates for BTR.

- Market Intelligence: Providing insights into local market dynamics, supply-demand imbalances, and competitive landscapes.

Currency Risk Management: Developing currency risk management programs to address AUD/EUR exchange rate volatility and protect EUR-denominated returns would be important considerations:

- Hedging Mechanisms: Financial instruments such as forward contracts could be used to lock in exchange rates for future income streams and principal repayments.

- Operational Hedging: Natural hedging opportunities within investment structures or operational practices could help balance currency exposures.

- Monitoring: Interest rate differentials between Australia and the Eurozone would influence hedging costs and effectiveness.

Operational Due Diligence: Focus on BTR and PBSA developments that demonstrate professional property management, tenant satisfaction, community building, and sustainable building practices. These operational factors may translate into lower tenant turnover, higher occupancy rates, and stable cash flows.

Policy Monitoring: Continuous monitoring of Australian government policy developments, particularly those related to international student migration and BTR incentives, would be important given the supportive but evolving policy environment.

By considering these factors, European private credit funds can evaluate the complexities and potential opportunities presented by Australia's rapidly maturing BTR and PBSA sectors.