The Bondification of Housing

by Ash Thomson, Founder

The Bondification of Housing: A data driven report unpacking the long-term value thesis for Australian BTR and PBSA investment.

I. Executive Summary: A Secular Shift in Real Estate Investment

This report advances the thesis that residential real estate is undergoing a multi-century structural transformation, shifting from a high-return, capital growth-driven asset to a stable, income-generating, "bond-like" asset class. This "bondification" is not a recent phenomenon but a long-term reversion to the historical mean, where rental yield, not price speculation, is the primary and most reliable source of total returns. The academic research underpinning this analysis, which reconstructs global housing data over nearly five centuries, provides a new lens through which to evaluate the future of residential investment, moving beyond the recency bias of the post-war era.1

This secular shift creates a powerful, long-term tailwind for Australia's nascent Build-to-Rent (BTR) and maturing Purpose-Built Student Accommodation (PBSA) sectors. These institutional-grade "living sectors" are intrinsically designed to capture the stable, inflation-hedged income streams that define the future of residential investment. As traditional avenues for capital appreciation diminish in line with historical norms, the focus for institutional capital must pivot towards assets that offer durable, predictable cash flow.

The key findings of this report are as follows:

- Historical data over nearly five centuries reveals that capital gains are a minor, volatile component of total housing returns, while rental yields provide the vast majority of stable, long-term value. On a global basis from 1560-2020, rental yields accounted for approximately 97% of real total returns.1

- The perception of a "housing boom" in recent decades is largely a valuation effect created by a secular, multi-century decline in discount rates, which has mechanically inflated asset prices. The analysis suggests that, relative to this trend, housing has often been valued at a discount, challenging the narrative of a persistent bubble.1

- Australia's BTR and PBSA sectors are uniquely positioned to thrive in this new paradigm. Their growth is supported by a chronic structural undersupply of housing, robust demographic tailwinds including strong overseas migration, and an increasingly favourable policy environment designed to attract institutional capital.2

- The primary valuation metric for these assets will shift from speculative growth forecasts to the yield spread over the Australian 10-year government bond, offering a clear, quantifiable measure of risk and return. A sustained long-term cap rate compression for these sectors is forecast as they de-risk, mature, and attract a deeper pool of institutional capital.

In conclusion, BTR and PBSA are not merely alternative asset classes; they represent the logical and necessary evolution of residential investment in Australia. They offer a scalable, professionalised vehicle for institutions to access the asset class's most reliable source of long-term value: stable, growing rental income. For investors prepared to look beyond the anomalous trends of the past half-century and embrace the long-term data, these sectors offer a compelling, defensive, and structurally supported opportunity.

II. The 'Bondification' of Housing: Unpacking the Long-Term Thesis

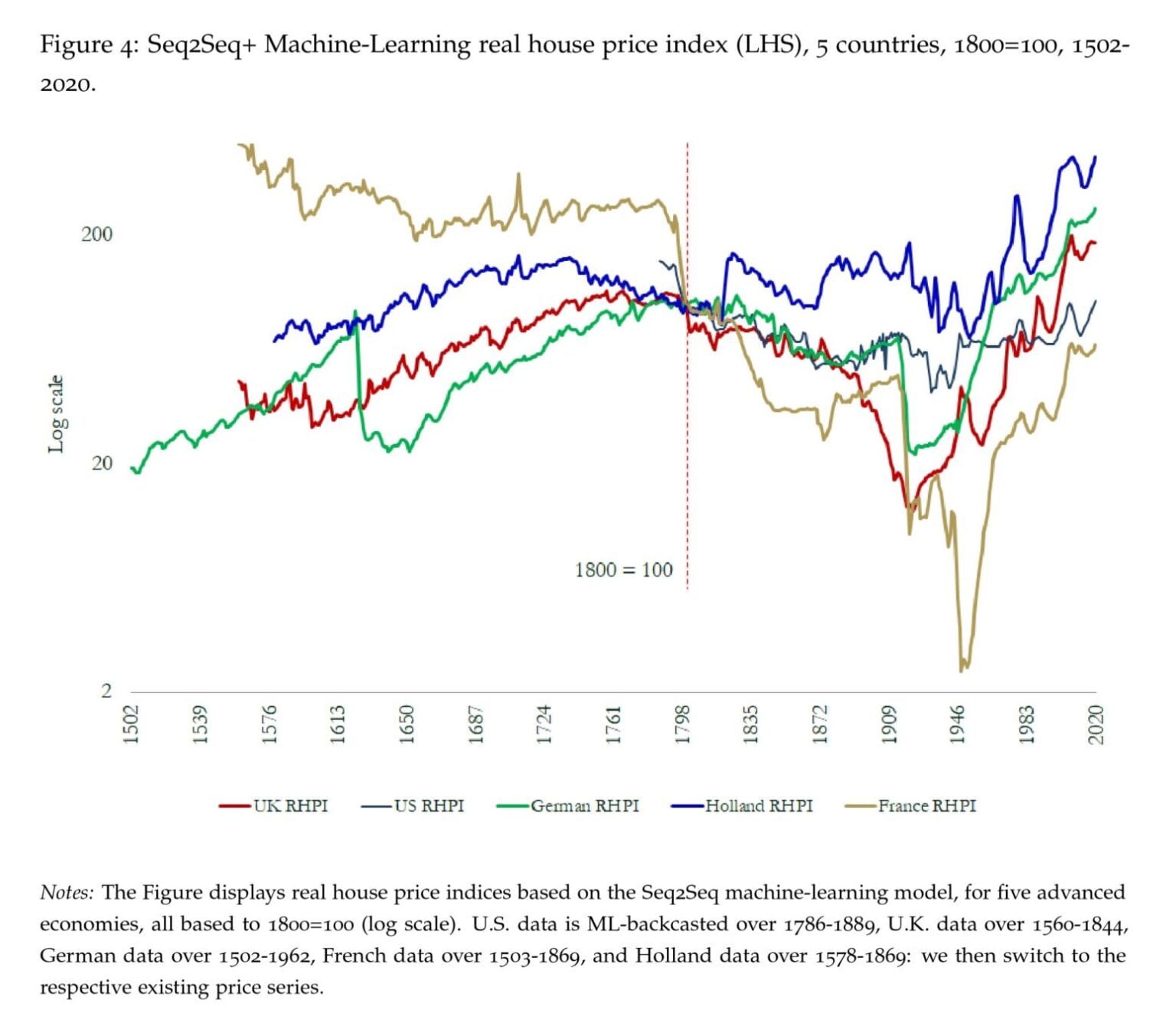

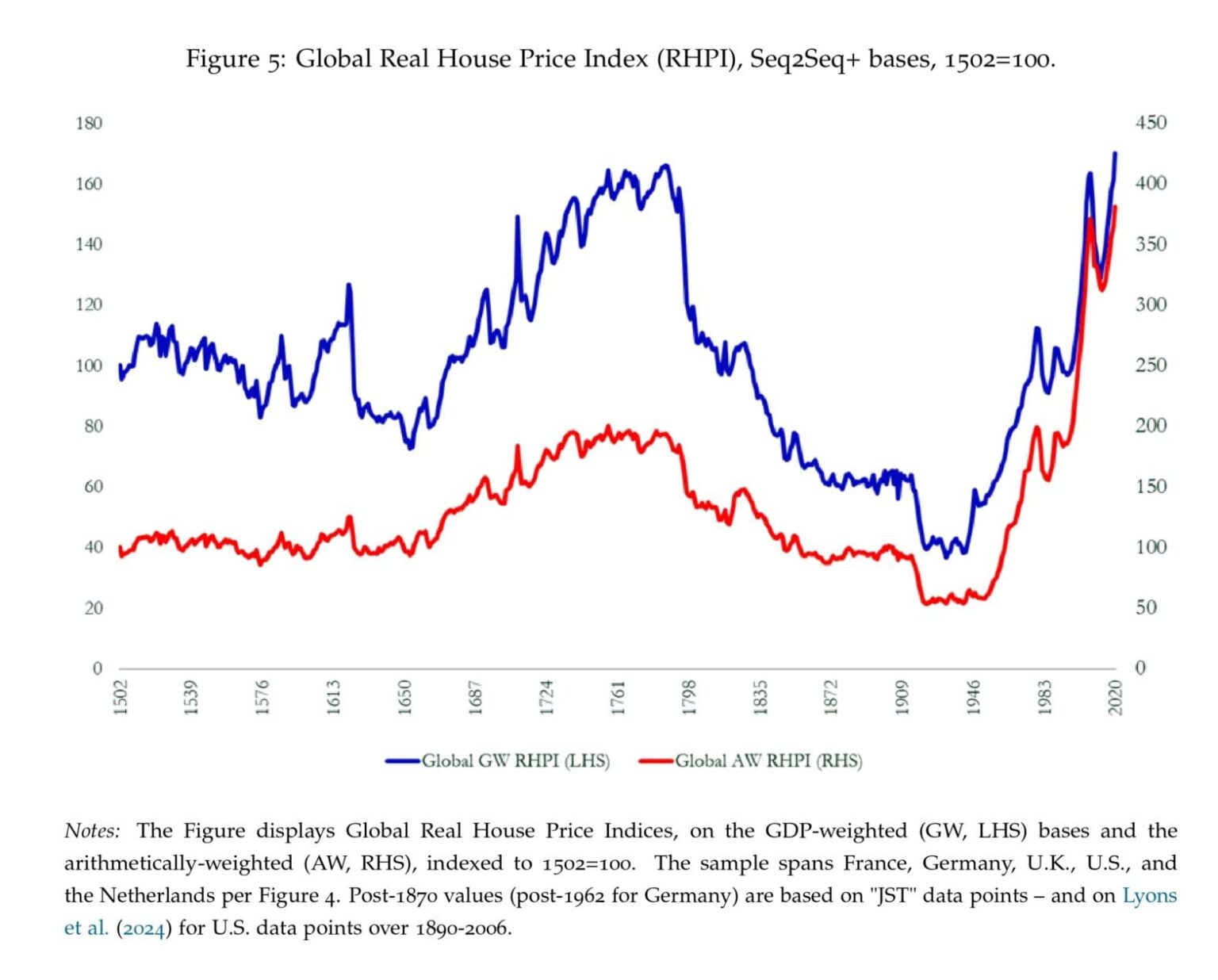

To understand the investment thesis we're presenting here for Australia's BTR and PBSA sectors, it is essential to first understand the profound, long-term structural shifts occurring within the global residential real estate asset class. Groundbreaking research by Paul Schmelzing (Stanford University), which reconstructs global housing returns from 1465 to 2024, challenges the modern consensus and re-establishes a historical, income-centric perspective.1 This research reveals that the characteristics of housing as an investment are converging with those of a long-duration bond—a process this report terms the "bondification" of housing.

A. The Primacy of Income: Deconstructing Total Returns Over Centuries

The modern investor's psyche is heavily conditioned by the experience of the post-World War II era, a period marked by substantial capital appreciation in residential property. This has led to a widespread belief that capital gains are the primary engine of real estate returns. However, the long-term data presents a starkly different reality.

The core finding from the multi-century analysis is that total returns from housing have been historically dominated by rental yield, with capital gains representing a far smaller and more volatile component.1 As demonstrated in Table 1, which summarises the global data from 1560 to 2020, the average real total return was approximately 6.3% per annum. Of this, rental yield contributed an overwhelming 6.1% per annum, while real capital gains accounted for a mere 0.2% per annum.1 This decomposition holds true across various historical epochs. Even during the period of 1960-2020, which saw the highest contribution from capital gains (1.7% p.a.), rental yield still provided the majority of the total return at 5.1% p.a..1

This fundamentally challenges the modern investment thesis. The long-term data suggests that an investment strategy predicated on speculative capital appreciation is misaligned with the fundamental, long-run character of the asset class. Periods of high capital growth are historical anomalies, not the norm. Therefore, a prudent long-term investor should view capital gains as an unpredictable bonus, while focusing on the stability and predictability of the rental income stream as the core driver of value. The German primary source data, constructed from archival repeat-sales records from 1465, provides an even more compelling case. In this granular, bottom-up series, long-run real total returns of approximately 5.9% per annum were composed of ~5.5% from rental yield and only ~0.4% from capital gains, reinforcing the global findings with meticulous archival evidence.1

| Period | Nominal TR | Real TR | Real Capital Gains | Rental Yield |

|---|---|---|---|---|

| 1560-1660 | 7.3% | 5.9% | -0.1% | 6.0% |

| 1660-1760 | 8.0% | 7.6% | 0.7% | 6.9% |

| 1760-1860 | 6.3% | 4.7% | -0.7% | 5.4% |

| 1860-1960 | 9.5% | 6.9% | 0.1% | 6.8% |

| 1960-2020 | 10.6% | 6.8% | 1.7% | 5.1% |

| Total (1560-2020) | 8.1% | 6.3% | 0.2% | 6.1% |

Source: Adapted from Schmelzing (2025), "Global Housing Returns, Discount Rates, and the Emergence of the Safe Asset, 1465-2024".1 All figures are GDP-weighted and per annum.

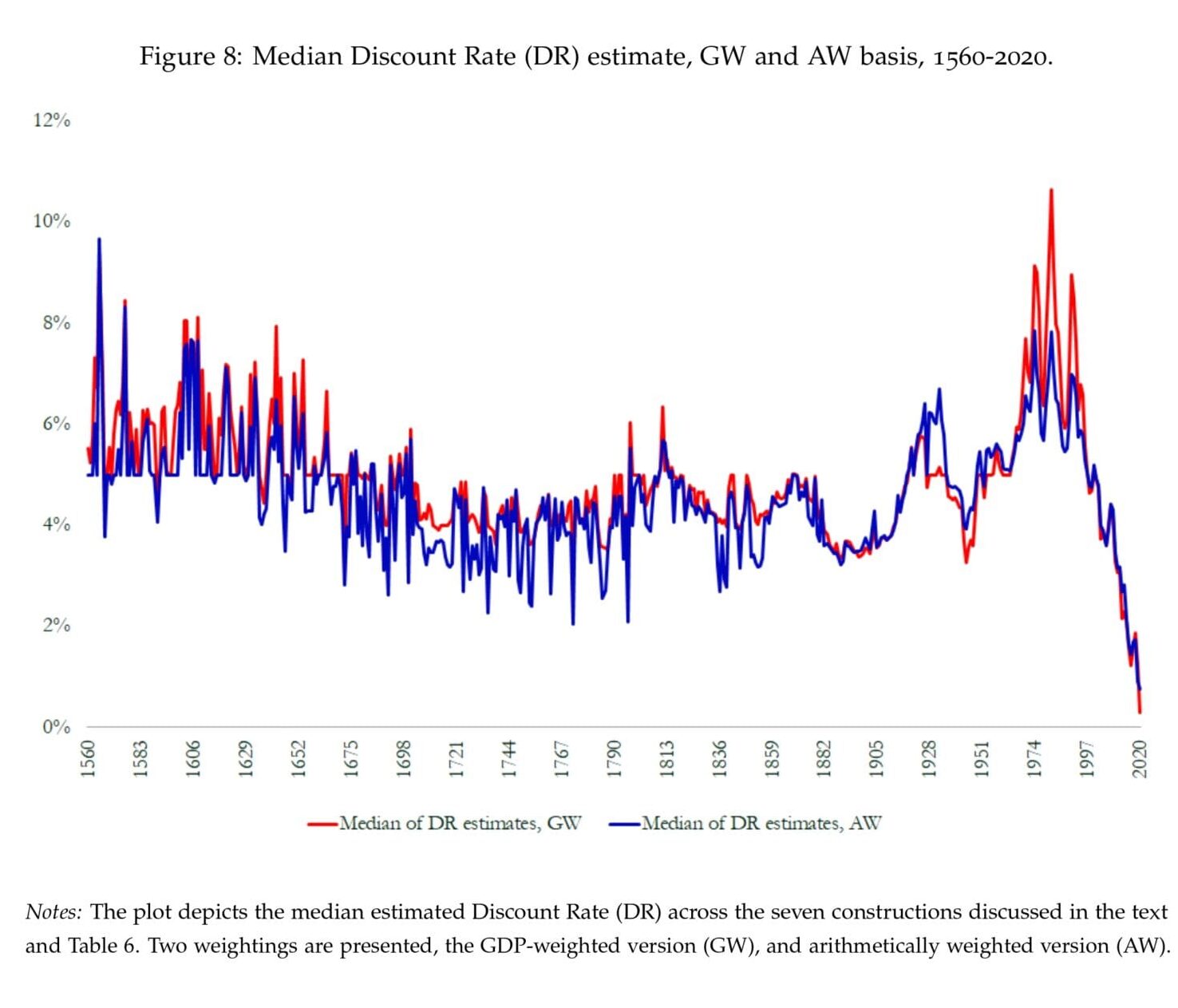

B. The Secular Decline in Discount Rates: The Engine of Modern Valuation

If capital gains are not the fundamental long-term driver of value, what explains the dramatic rise in house prices observed in many advanced economies over the past century? The research provides a compelling answer: a clear, multi-century downward trend in housing discount rates.1

Housing, with its long-term stream of rental income, can be valued like any other cash-flow-generating asset using a present value model. The research demonstrates that the primary driver of rising housing valuations has not been a surge in expected future rent growth, but rather a prolonged fall in the rate at which those future rents are discounted.1 As discount rates fall, the present value of the entire future rental stream increases, mechanically pushing up the asset's capital value. This creates the illusion of a fundamental "boom."

This analysis is supported by newly constructed multi-century data for mortgage rates—arguably the most relevant discount rate for housing—which also exhibit a clear secular downward trend.1 The implication of this finding is profound. The paper argues that when comparing the actual rise in house prices to the implied rise based on falling discount rates, housing in advanced economies has often been valued at a discount in recent decades.1 This suggests that the run-up in prices is not necessarily an irrational bubble, but a rational, if perhaps incomplete, repricing in response to a structurally lower cost of capital.

For investors, this means that the tailwind of falling discount rates, which has provided a significant boost to capital values for decades, cannot be expected to continue at the same pace indefinitely. Future returns will therefore be even more reliant on the underlying income characteristics of the asset, reinforcing the need to temper expectations for capital appreciation. The analysis reveals that housing behaves much like a long-duration bond: its value is highly sensitive to changes in long-term interest rates, as its worth is derived from a very long-term stream of cash flows. This perspective shifts the asset's position within a portfolio away from speculative growth categories and towards stable, duration-matched assets like infrastructure and long-term government bonds.

C. The Rental Yield-Sovereign Spread: A New Barometer for Housing Value

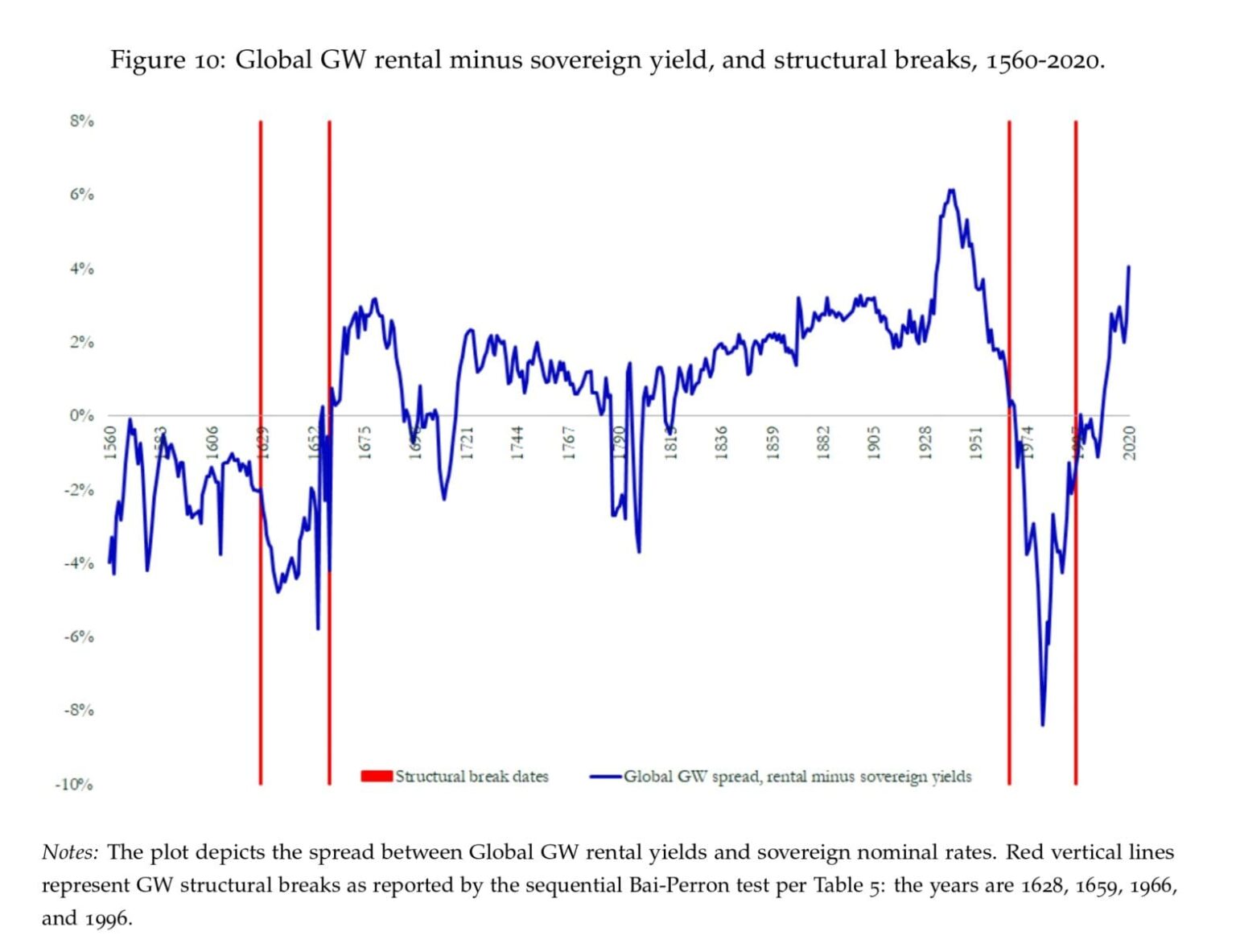

The historical analysis also provides a powerful framework for the relative valuation of housing. The research pinpoints a critical inflection point in the mid-to-late 17th century. Prior to this, sovereign bond yields often traded above housing rental yields. However, around the 1660s, a structural crossover occurred, and sovereign yields fell sustainably below rental yields.1 This marked the emergence of sovereign bonds as the premier "safe asset," an asset so secure that investors were willing to accept a lower yield in exchange for its safety and liquidity—a phenomenon now known as the "safety premium".1

Consequently, the positive spread of rental yield over the sovereign yield represents the risk premium that investors demand for holding a less liquid, less secure, and more management-intensive asset like property. This spread is not static; the data shows it has been secularly increasing over time, reflecting the growing safety and liquidity of sovereign debt relative to housing.1

This historical framework provides an invaluable tool for modern investors. It suggests that the most logical and disciplined way to assess the value of residential real estate is by benchmarking its income yield against the risk-free rate offered by government bonds. This moves the valuation discussion away from unreliable and speculative forecasts of future price movements and towards a rigorous, relative-value approach. When the spread between rental yields and sovereign yields is unusually tight, it signals that investors are not being adequately compensated for the additional risks of holding property, and future returns are likely to be unattractive. Conversely, a wide spread indicates a compelling entry point where the risk premium is high. This disciplined approach is central to navigating the "bondified" real estate landscape of the 21st century.

III. The Bull Case for Australian Build-to-Rent (BTR): An Asset Class for the New Paradigm

The secular, global shift of housing towards a bond-like, income-driven asset class provides the foundational context for a powerful, long-term bullish thesis for Australia's Build-to-Rent (BTR) sector. BTR is not merely a new development model; it is an institutional asset class whose fundamental characteristics are perfectly aligned with this new investment paradigm. While the broader residential market grapples with the end of an era of easy capital gains, BTR is purpose-built to thrive by focusing on the most durable source of long-term value: stable, growing rental income.

The Australian BTR market is at a critical inflection point. As shown in Table 2, the sector is rapidly scaling from a small base, supported by powerful demand drivers and an increasingly favourable policy landscape.

| Metric | Build-to-Rent (BTR) | Purpose-Built Student Accommodation (PBSA) | Data Source Snippet(s) |

|---|---|---|---|

| Operational Units/Beds | 10,276 units (Q1 2025) | ~122,000 beds6 | |

| Under Construction | 11,582 units (Jan 2024) | ~16,000 beds7 | |

| Planning Pipeline | 32,910 units (Jan 2024) | ~8,000 approved, ~13,200 in planning7 | |

| Total Pipeline Size | ~65,575 units (Q1 2025) | ~35,605 beds in total pipeline6 | |

| Estimated Market Value | ~$39bn (completion value of pipeline) | N/A (Major transactions >A$2.3bn in 24 mos)8 | |

| Institutional Penetration | 0.2% of total rental supply | 6.4% of student housing4 | |

| Key Demand Drivers | Housing crisis, low vacancy (~1%), population growth, declining affordability | World-class education, international student growth (>1m), structural undersupply2 | |

| Key Government Incentives | MIT withholding tax reduced to 15%; Capital works deduction increased to 4% | Recognised as alleviating rental pressure; calls for accelerated development pathways13 |

A. Structural Alignment: A Model Built for Income, Not Speculation

The very definition of BTR aligns it perfectly with the "bondification" thesis. BTR involves the development and long-term ownership of large-scale residential assets by a single institutional entity, with the prime business objective being the generation of a secure and predictable income stream.15 This stands in stark contrast to the traditional Australian rental market, which is dominated by a fragmented base of small-scale "mum and dad" investors who are often motivated primarily by capital gains and negative gearing benefits.4

The BTR model is a pure play on maximising Net Operating Income (NOI). Its success is not dependent on speculative market timing but on operational excellence: professional on-site management, high-quality amenities to attract and retain tenants, efficient cost control, and the ability to capture market rental growth.16 This focus on the underlying cash flow of the asset is precisely what the long-term historical data suggests is the most reliable path to value creation in residential real estate. The fragmented nature of the existing rental market has made it virtually impossible for large institutions to gain scalable exposure to this income stream. BTR solves this fundamental problem by creating large, high-quality, institutional-grade assets, thereby unlocking the multi-trillion-dollar residential sector for long-term institutional capital that has historically been excluded.2

B. The Demand-Side Imperative: A Deep and Durable Income Stream

The investment case for BTR in Australia is underpinned by some of the strongest and most durable demand fundamentals of any real estate sector in the developed world. These factors create a powerful, long-term support mechanism for the rental income streams that BTR assets are designed to capture.

First, Australia is in the midst of a severe and structural housing crisis. The nation faces a significant supply deficit, with forecasts from the National Housing Finance and Investment Corporation pointing to a shortfall of over 106,000 dwellings by 2026.19 To address this, the Federal Government has set an ambitious target of building 1.2 million new homes by 2029 under the National Housing Accord, a goal that many analysts believe is unlikely to be met through traditional development models alone.3 This chronic undersupply provides a powerful, long-term support for rental demand and, consequently, rental growth.

Second, this supply crisis has driven rental market conditions to historic extremes. National rental vacancy rates are hovering at or near record lows of around 1%, far below the 3% level typically considered a balanced market.4 This intense competition for rental properties has fueled an unprecedented surge in rents. Since March 2020, national rents have climbed by a staggering 38.4%, and leading forecasts project a further 25% increase over the next five years.21 This provides a clear and visible pathway for strong NOI growth in BTR assets for the foreseeable future.

Third, long-term demographic and social trends are creating a structural shift towards renting. Strong population growth, driven by a rebound in overseas migration, is a primary source of new rental demand.4 Concurrently, declining housing affordability, exacerbated by the rapid rise in dwelling values and higher interest rates, is pushing the dream of homeownership out of reach for many. The average age of a first-home buyer in Australia is now approaching 40, creating a deep and growing cohort of long-term, non-discretionary renters.4 These are no longer just students or young professionals in a transitional phase; they are established households and families seeking stable, high-quality rental accommodation, the precise demographic that institutional BTR is designed to serve.

C. The Supply-Side Enablers: Institutional Capital Meets Policy Support

While the demand case is compelling, the viability of a new asset class depends equally on the availability of capital and a supportive regulatory environment. On both fronts, the Australian BTR sector has reached a positive inflection point.

Historically, punitive tax settings—particularly at the state level regarding land tax and at the federal level concerning the Managed Investment Trust (MIT) withholding tax for foreign investors—made BTR financially unfeasible compared to other commercial property asset classes.15 This created a significant barrier to entry. However, the escalating housing crisis has forced a fundamental policy pivot. Recognizing that institutional investment is a critical part of the supply solution, the Federal Government has introduced landmark tax incentives.2 The two most significant changes are the reduction of the MIT withholding tax for foreign investors in eligible BTR projects from 30% to 15%, and an increase in the annual capital works depreciation rate from 2.5% to 4%.13

These incentives are game-changers. They directly address the historical tax disadvantages, materially improve project feasibilities, and enhance investor returns. This policy support acts as a powerful de-risking mechanism, sending a clear signal to global capital that Australia is "open for business" in the BTR sector. This has been met with a surge in institutional interest. The sector is attracting significant capital, particularly from experienced foreign investors from the mature US and UK markets who are familiar with the model's defensive characteristics.3 Over $5 billion in capital was raised to support the Australian BTR sector in 2023 alone, providing the fuel for the sector's rapid expansion from its current nascent stage.26 While it currently represents just 0.2% of Australia's rental supply, its growth trajectory is mirroring that of the UK in the early 2010s, with immense potential to scale towards the penetration rates seen in mature markets like the US (12%) and UK (5.4%).4

IV. The Enduring Appeal of Purpose-Built Student Accommodation (PBSA): A Mature Precedent

While BTR is a relatively new concept in the Australian institutional landscape, the underlying model of large-scale, income-focused residential investment is not. The Purpose-Built Student Accommodation (PBSA) sector serves as the established forerunner to BTR, providing a powerful proof of concept and a rich data set that de-risks the investment thesis for the broader "living sectors."

A. PBSA as Australia's BTR Archetype

The Australian PBSA market is a mature and well-established institutional asset class. It has a track record spanning over 15 years and comprises over 122,000 operational beds, with a further 16,000 under construction.7 This sector provided the first successful blueprint for developing, operating, and attracting institutional capital into large-scale, professionally managed residential assets in Australia.

The maturity of the market has been validated by significant transactional activity from major global players. The landmark acquisition of a 5,662-bed portfolio by Greystar for A$1.6 billion in late 2024 is a testament to the sector's institutional appeal and highlights strong confidence in its long-term fundamentals.27 This history of successful investment and operation provides a crucial precedent for BTR. It demonstrates that the model of professionally managed, amenity-rich rental housing can thrive in the Australian context, giving new investors in BTR confidence in the operational assumptions—such as lease-up rates, operating costs, and achievable rents—that underpin their financial models. The lack of a local operational track record is often cited as a key barrier for institutional capital entering a new market.18 The Australian PBSA market provides over a decade of transparent, real-world data that can be used as a reliable proxy to underwrite BTR investments, significantly reducing the perceived risk and accelerating capital deployment.

B. Resilient Demand and Global Hub Status

Similar to BTR, the investment case for PBSA is founded on a deep and structural undersupply. Australia has a low provision rate of student beds compared to global peers like the UK and US, with estimates of the student-to-bed ratio as high as 16:1.7 In Melbourne's core university precinct alone, there is an estimated unmet demand for circa 10,000 PBSA beds.29

The demand drivers for PBSA are exceptionally resilient and often counter-cyclical. The sector's health is intrinsically linked to Australia's world-class higher education system, which functions as one of the nation's largest export industries.30 International student enrolments have rebounded dramatically since the pandemic, exceeding 1 million in 2024—well above pre-COVID levels.10 This demand is less correlated with the domestic economic cycle, providing a defensive and stable income stream for investors, a particularly attractive quality in times of economic uncertainty.

Furthermore, policymakers and stakeholders increasingly view PBSA not just as student infrastructure, but as a critical component of the solution to the broader housing crisis.14 Every student housed in a PBSA bed is one less person competing in the extraordinarily tight private rental market. This alignment with public policy goals ensures strong ongoing social and political support for the sector's continued growth, with calls for accelerated development pathways to bring more supply online.14 This symbiotic relationship between public need and private investment creates a durable and supportive operating environment for the sector.

The growth of both BTR and PBSA is mutually beneficial. They attract the same pools of sophisticated global institutional capital and are often grouped together as the "living sectors".33 As BTR scales, it creates a larger, more liquid, and better-understood living sector market overall. This, in turn, enhances the attractiveness of the existing PBSA market for investors seeking scale, diversification, and operational synergies, creating a virtuous cycle where growth in one sub-sector enhances the investment case for the other.

V. Implications for Capitalisation Rates and Long-Term Valuation

The "bondification" of housing necessitates a fundamental shift in how residential assets like BTR and PBSA are valued. The focus moves away from speculative capital growth forecasts and towards a more disciplined analysis of income yield relative to the risk-free rate. This section provides a quantitative framework for this approach and forecasts the long-term trajectory of capitalisation rates for these sectors in Australia.

A. The New Benchmark: The Spread to Sovereign Bonds

The primary benchmark for any "bond-like" asset is the yield on a long-term government bond, which represents the risk-free rate of return. In Australia, the 10-year government bond yield has been trading in a range of 4.2% to 4.3% through mid-2025.34

Against this benchmark, income-producing real estate must offer a "yield spread" or "risk premium" to compensate investors for factors such as illiquidity, management intensity, and credit risk (the risk of tenant default). Transactional evidence from the mature PBSA sector shows cap rates are currently in the 5.0% to 5.5% range.10 While the BTR market has fewer transactional data points, its similar risk-return profile suggests cap rates will settle in a comparable range.

This establishes an initial yield spread for the institutional living sectors of approximately 75 to 125 basis points (bps) over the 10-year government bond. This spread will become the primary valuation metric for the sector. A stable spread in the vicinity of 100-150 bps would offer a compelling return for a de-risked, institutional asset class that also provides an income stream with an implicit link to inflation, attracting long-term, liability-matching capital from sources like pension funds and insurance companies.

| Asset Class | Indicative Cap Rate / Yield | Australian 10-Year Bond Yield | Implied Yield Spread (bps) | Commentary / Forecast |

|---|---|---|---|---|

| Purpose-Built Student Accommodation (PBSA) | 5.00% - 5.50% | ~4.25% | 75 - 125 bps | Stable, counter-cyclical demand. Mature asset class. Forecast long-term compression. |

| Build-to-Rent (BTR) | 5.00% - 5.75% (Emerging) | ~4.25% | 75 - 150 bps | Nascent market with higher initial risk premium. Strongest potential for compression as sector de-risks. |

| Prime Sydney Office (for comparison) | ~5.25% - 5.75% | ~4.25% | 100 - 150 bps | Facing structural headwinds (remote work). Higher risk premium reflects uncertain income growth. |

| Prime Melbourne Industrial (for comparison) | ~4.75% - 5.25% | ~4.25% | 50 - 100 bps | Strong fundamentals but yields already compressed. Lower spread reflects lower perceived risk. |

Note: Cap rates and yields are indicative for H2 2025 based on market reports and forecasts. Bond yield is as of mid-2025. Sources:.10

B. The Path to Long-Term Cap Rate Compression

A key component of the bullish thesis for BTR and PBSA is the strong potential for long-term cap rate compression, which would deliver significant capital growth to early investors. This compression is expected to be driven by two powerful, converging forces: a falling risk-free rate and a tightening risk premium.

First, there is a strong market consensus that the Reserve Bank of Australia will commence a monetary policy easing cycle in late 2024 or early 2025 in response to moderating inflation.22 This is forecast to lead to a decline in the 10-year government bond yield, with some analysts predicting it will settle in a long-term range around 3.5% from mid-2026 onwards.35 A structural decline in the risk-free rate will exert powerful downward pressure on all property yields, including BTR and PBSA.

Second, as the BTR and PBSA sectors mature in Australia, their perceived risk profile will decrease, leading to a tightening of the required risk premium (the yield spread). This de-risking will occur through several channels:

- Scale and Liquidity: As the total value of the BTR/PBSA market grows from tens of billions to a forecast potential of over A$290 billion, it will create a deep and liquid market, reducing the illiquidity premium investors currently demand.19

- Transactional Evidence: A greater volume of transactions will provide clear pricing benchmarks, reducing valuation uncertainty and giving institutional trustees more confidence to invest.2

- Operational Track Record: As more assets become operational and stabilise, a rich local data set on performance will emerge, reducing uncertainty around underwriting assumptions.8

Combining these factors, a long-term cap rate compression of 60 to 100 basis points is forecast for both BTR and PBSA over the next five to seven years.22 This provides investors with a dual source of total return: a stable, growing income yield plus the potential for significant capital appreciation driven by this structural repricing. This presents a classic "first mover advantage," where early investors are positioned to capture both a relatively high initial yield and the subsequent capital growth from compression as the market matures.38

Crucially, the valuations of BTR and PBSA are expected to be more resilient than those of traditional commercial real estate sectors like office and retail. The income streams underpinning BTR and PBSA are driven by non-discretionary human needs—shelter and education—and are supported by long-term demographic trends rather than cyclical business investment or consumer spending.4 In an economic downturn, this defensive characteristic should lead to more stable income and, therefore, more resilient valuations, justifying a tighter long-term yield spread to bonds compared to more cyclical property types.

VI. Conclusion: The Future of Australian Residential Investment

The multi-century data presented in this report is unequivocal: residential real estate is, at its core, an income-producing, bond-like asset. The speculative, capital-growth-focused mindset that has dominated the last 50 years was a historical anomaly, fueled by a secular decline in interest rates that cannot be repeated. As this era concludes, the market is returning to first principles, where long-term value is derived not from forecasting price bubbles, but from the quality, stability, and durability of cash flow.

In this new (or rather, old) paradigm, Build-to-Rent and Purpose-Built Student Accommodation are not niche alternatives. They are the institutional vanguard, providing the professionalised, scalable platforms necessary to invest in residential property based on its true, long-term characteristics. They offer a direct, market-based solution to Australia's acute housing crisis while providing investors with stable, inflation-hedged, bond-like returns. These returns are supplemented by the significant potential for long-term capital growth, driven not by speculation, but by a structural and foreseeable compression in capitalisation rates as these sectors mature.

For long-term institutional investors, the strategic imperative is clear. The era of relying on broad-based, speculative capital appreciation across the residential market is drawing to a close. The future of institutional residential investment in Australia lies in the disciplined acquisition and development of high-quality, income-generating BTR and PBSA assets. These sectors offer a compelling and timely blend of defensive income and structural growth that is perfectly positioned for the decades to come.